Transform Your Bank or Credit Union with Business and Process Standardization

As an executive at a bank or credit union, you know that process-mapping your financial institution is the essential first step toward strategic transformation. (If you’d like to learn more about end-to-end or E2E process mapping for banks and credit unions, be sure to check out our informative article on that topic.)

We also have lots of great videos, typically about three minutes long, one the essential prerequisite topic of process mapping in banks and credit unions:

• Commercial lending e2E process mapping video

• Consumer lending E2E process mapping video

TRANSFORMATION-READINESS

Current-state process mapping for banks and credit unions: Required for transformation of your financial institution

So let’s assume, for this article, that you—and your internal improvement teams and technology leads—have got all your bank or credit union’s internal processes and customer or member journeys properly mapped, down to the individual activity level of detail. (And when it comes to robotic process automation or RPA in credit unions and banks, processes must often get mapped down to the individual keystroke level of detail.)

We’ll start with the assumption, then, that you possess a good baseline understanding of how your organization currently operates, based on your successful E2E process mapping.

Now it’s time to transform. And this applies to everything from standardizing business processes, to introducing (or accelerating and/or expanding) AI and robotic process automation or RPA, and upgrading your advanced analytics with cleaner data, or what you might call “a more singular source of truth.”

But before we dive into the benefits of business and process transformation for credit unions and banks, let’s address some of the challenges you’re surely aware of… and some others that might be lurking under the radar.

TYPICAL CHALLENGES TO TRANSFORMATION

What are the challenges of business and process transformation in financial institutions such as banks and credit unions?

“It’s too hard. We’ve tried, and failed, too many times before.” Business and process transformation, in the eyes of many C-level leaders at banks and credit unions, is simply daunting. Executives perceive it as difficult, and often have the scars to prove it.

Too much seems to be at stake. So many leaders tend to over-invest in project management via over-engineering of tasks. As a result, the benefits, if any, are intangible and/or theoretical. Many execs thus end up with the sour aftertaste of buyer’s remorse, wondering why they’d attempted the transformation in the first place.

Let’s parse the actual challenges that face any bank or credit union executive as they embark on a transformation journey. Basically, there are three:

Bank/Credit Union Transformation Challenge 1: “How do I begin?”

Transformation is especially daunting when the situation itself is opaque. Executives often ask—or perhaps complain—”Where do I start? I don’t even know what’s going on in my organization.”

As you likely have intimated by the points made at the beginning of this article, process mapping should always be Step One on your strategic roadmap toward transformation. Again, check out our great article, “Process Mapping and Improvement for Banks and Credit Unions” on that topic.

Once you complete end-to-end (or “wall-to-wall”) process mapping in your financial institution, whether it’s a bank or credit union, you’ll quickly emerge from the darkness. You’ll know exactly what’s going on in your organization, including not only what’s happening, but what’s working, what’s not, why, and what’s needed. Talk about a prerequisite to transformation in banks and credit unions.

So Challenge 1 is certainly a real one, but it’s also surmountable.

Bank/Credit Union Transformation Challenge 2: “How do I prioritize improvements?”

This is a great question. End-to-end process-mapping of your credit union or bank likely yielded an inventory of hundreds of improvements, both incremental and large-scale, that could be implemented:

- They could be basic, such as creating or standardizing templates for routine tasks.

- They could be more comprehensive, such as implementing front-end agentic AI agents to trigger back-end robotic process automation in banking, also known as RPA. An example: overhauling the front end of the process with new interface (power apps) and other automation to minimize multiple screens and tabs.

So where do you start? How do you prioritize? Each one seems as urgent as the next. Every single improvement will deliver value. And they can all bestow greater customer/member and employee satisfaction.

It may sound simplistic, but the answer is: Start at the beginning.

Put it this way: The intake of any end-to-end business process has impact downstream. It’s more than just “impact”; think “snowballing.” Everything that you clean up, up front, delivers multiples of benefits to downstream processes and work activities.

Here’s a good example. Think of the process by which customers or members apply for loans, whether they’re commercial or residential. If you can have a clearly-defined set of data and documents to collect at all stages of the application process, with proper permutations for all the different products, customers, and risk levels, you will:

- Reduce the pain points—for both customers/members and employees—throughout the process.

- Reduce rework by a staggering 25 to 40 percent.

- Scale the process itself, buying you time to actually work on the follow-up automations to sustain and maintain the original improvement.

Not bad for standardizing the “intake.”

“Starting at the start” gives you immediate relief. It drives momentum. And, perhaps best of all, it’s not nearly as complicated a process as you may think.

After that, it becomes a matter of lather/rinse/repeat… process-by-process, business-by-business.

Bank/Credit Union Transformation Challenge 3: “How can I transform without the resources—or time?”

Here’s welcome news: You don’t have to close your business to improve your business.

How is that possible? It is; we speak from experience. At The Lab, we’ve been transforming businesses (none of which were shut down in the process!) since 1993, all while keeping daily operations running and on-track.

Which begs the question: How?

The one-word answer is “Templates.” Over those three-plus decades, we have templatized every bank and credit-union process, data map, executive KPI, best practice, AI and automation requirement, and even code. It’s all been catalogued in The Lab’s proprietary Knowledge Base, informed by the IP from thousands of client engagements over the years.

This lets you effectively pick from a menu, which we’ll help you to prioritize, to begin the work. And since most of the improvements are drag-and-drop, you get them implemented—and start reaping the benefits—in a quarter of the time it typically takes an organization to transform.

Now think back to the solution to Challenge 2: Start at the beginning. This is the right way to effect a transformation in banks and credit unions. Starting at the beginning, as we will help you to do, you’ll immediately relieve resources which can in turn be channeled to the transformation work. It’s a virtuous cycle.

Don’t get us wrong; we’re not trying to sugar-coat this. We don’t want you to under-estimate that amount of oversight, management, and plain old elbow grease required to transform an organization as intricate and interconnected as your financial institution. It will be a grind. But rest assured: With the right prioritization, aligned with clear strategic goals, you’ll be transforming in no time.

SOURCES OF BENEFITS

What kinds of benefits can my bank or credit union get from business and process transformation?

By this point, you’re not daunted by the challenges. Transforming your bank or credit union is all about the benefits.

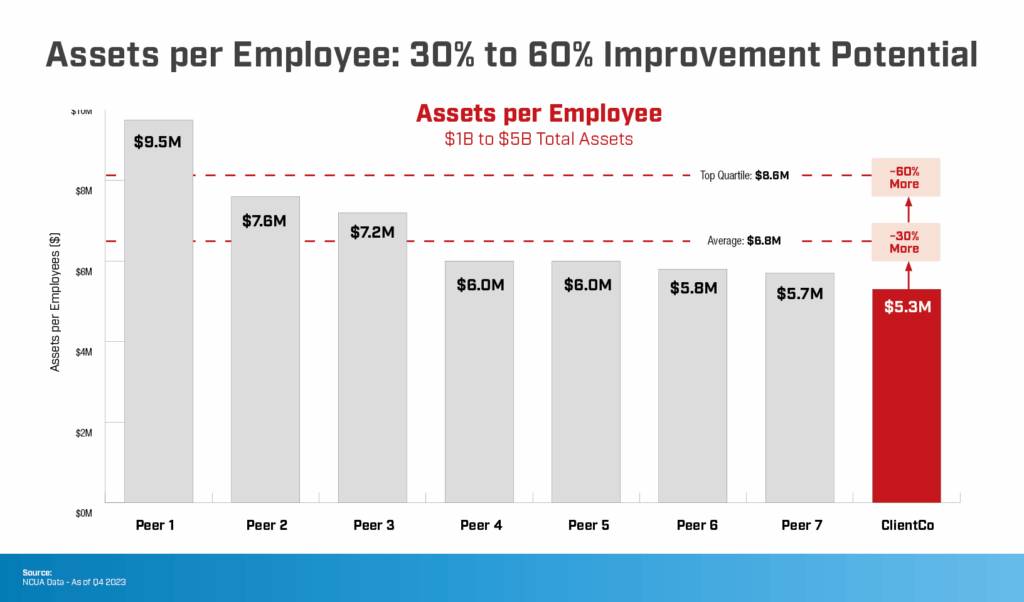

As an executive at a bank or credit union, you understand that operational efficiency drives both performance and profitability. Improving the bottom line, and delivering better customer or member experiences, starts with streamlining work to drive stronger results.

As we dive deeper into this article, you’ll see clear benefits, the types of services needed to transform, and real-world examples of how The Lab has helped banks and credit unions such as yours to improve efficiency, expand client relationships, and increase margin… in just six to 12 months.

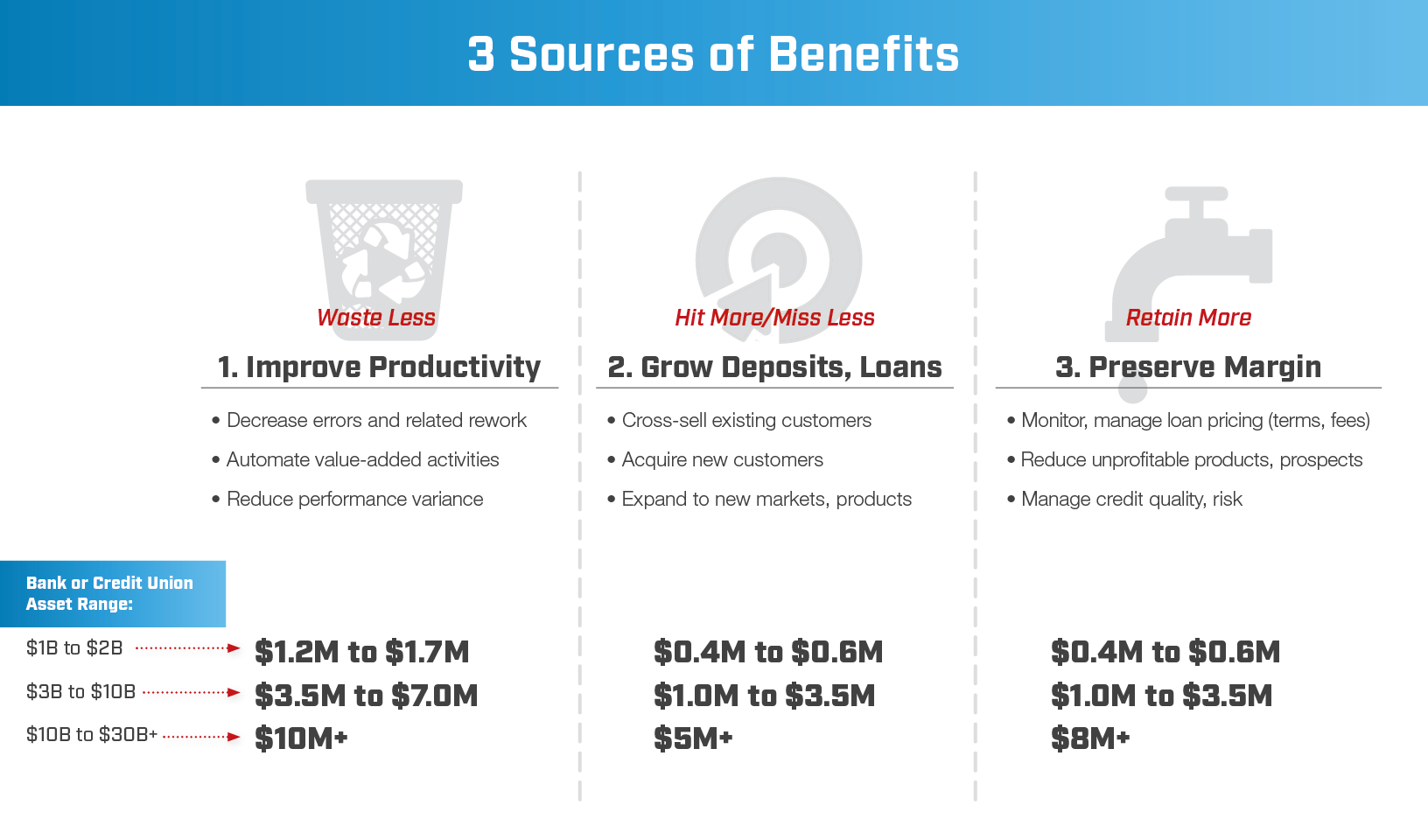

In order to reap the maximum return on your bank or credit union’s transformation effort, in the shortest amount of time, focus on these three major sources of benefits:

1. Waste less: Improve productivity.

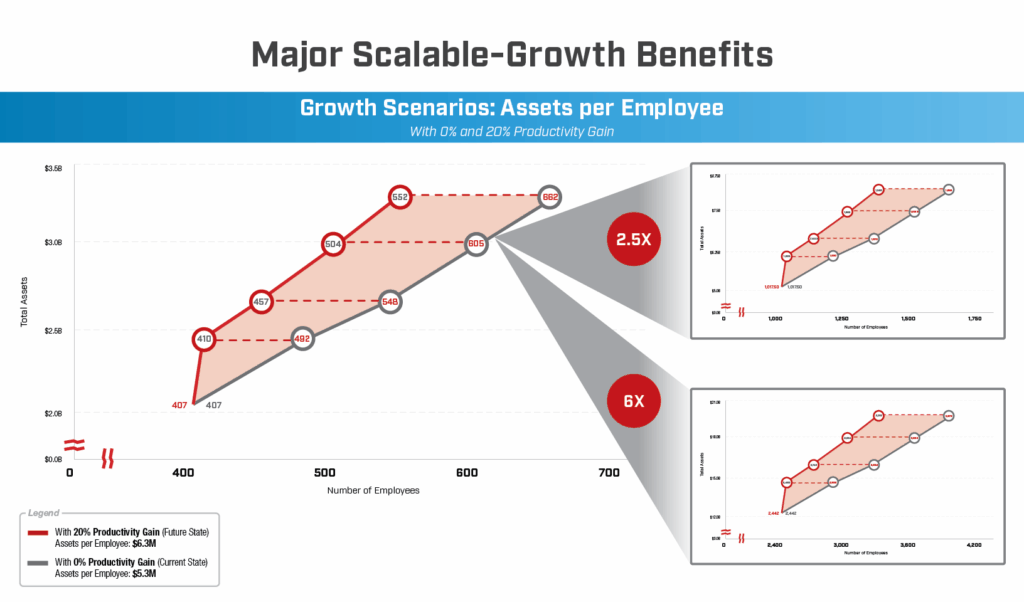

Many of the business and process-transformation improvements (detailed later in this article) will directly impact the step-by-step work activities performed each day by your team. The improvements will re-order, re-organize, and overall reduce the number of manual steps performed, courtesy of standardization and AI in banking with robotic process automation (RPA). Taken together, this can scale your organization’s capacity anywhere from 25 to 40 percent. Oh, and the “waste reduction” also translates to “error reduction.” Which translates to “better compliance” and “improved customer experience.” See what we mean about a virtuous cycle?

2. Hit more/miss less: Grow deposits and loans.

When you transform your bank or credit union’s business and its operational data, then advanced analytics and automation can serve all levels of management and the frontline staff with things like:

- Powerful customer segmentation models.

- Insights into existing customers’/members’ potential cross-sell opportunities.

- Actionable market and lead assessments for the teams to apply to their overall strategy and day-to-day operations.

3. Retain more: Preserve your margin

Here’s one that always makes bank and credit-union executives sit up and take notice: Armed with enhanced data intelligence, real-time margin by product/customer, accurate pricing of new deals, and streamlined credit-risk assessments, you can add a measurable three to five+ basis points to your bank or credit union’s bottom line.

(Want more tantalizing detail? Read all about the Banking Basis-Point Bot™ from The Lab.)

Remember: these are just sources of benefits you should pursue in your strategic transformation roadmap. There are even more, specific benefits to be had. That’s a teaser; we’ll share them with you later in this article.

How-To Transform (Step-by-Step)

How do you perform a business and process transformation in banks and credit unions?

Since 1993, The Lab has helped peer banks and credit unions transform, using our patented approach. And with the guidance we’ll describe below, you can, in less than a year, be able to see measurable improvements in KPIs and bottom-line margin.

In this long-form explanatory article about how to go about actually doing a business and process transformation in banks and credit unions, we’ll answer your top, burning questions:

- What am I actually transforming in my bank or credit union?

- Where do I need to begin transformation in my credit union or bank?

- Are there typical pitfalls and traps that we can avoid as we transform our bank or credit union?

- How can my bank or credit-union transformation deliver meaningful (and not just theoretical) benefits?

Let’s dive in.

1. What am I actually transforming in my bank or credit union?

There are three key business strategic areas that you want to transform, in order to delight your customers or members; build a more resilient, automated business; and boost your bottom line. They are:

- Business process standardization. Simply put, this means making business processes simpler and more consistent.

- Executive KPIs. This is all about data intelligence and the vital few key performance indicators or KPIs. The goal here is to transform (yes, “transform”!) data into actionable insights for leadership, management, and the front line.

- Enabling (more) automation capabilities. Operational excellence is part of your bank or credit union’s strategic transformation. Thus you want to unlock more automation to make human work easier.

While many bank and credit union business processes have evolved, and improved, over the years, thanks to the implementation of large platforms and new technologies, a dirty little secret persists: Humans are too often forced to act as the “glue” between systems that can’t, and don’t, talk to each other. Not surprisingly, traditional “process improvements” have yielded only minimal efficiency gains.

But when you transform your bank or credit union’s business processes—along with standardizing and improving the visibility of its Executive KPIs, supported by front-end automations that actually work—then you can truly transform the organization. And to do that, you’ll need to:

- Design a future-state process, end-to-end, for each business.

- Understand and detail the prerequisites to reach this future state.

- Prepare your data for automation readiness.

2. Where do I need to begin transformation in my credit union or bank?

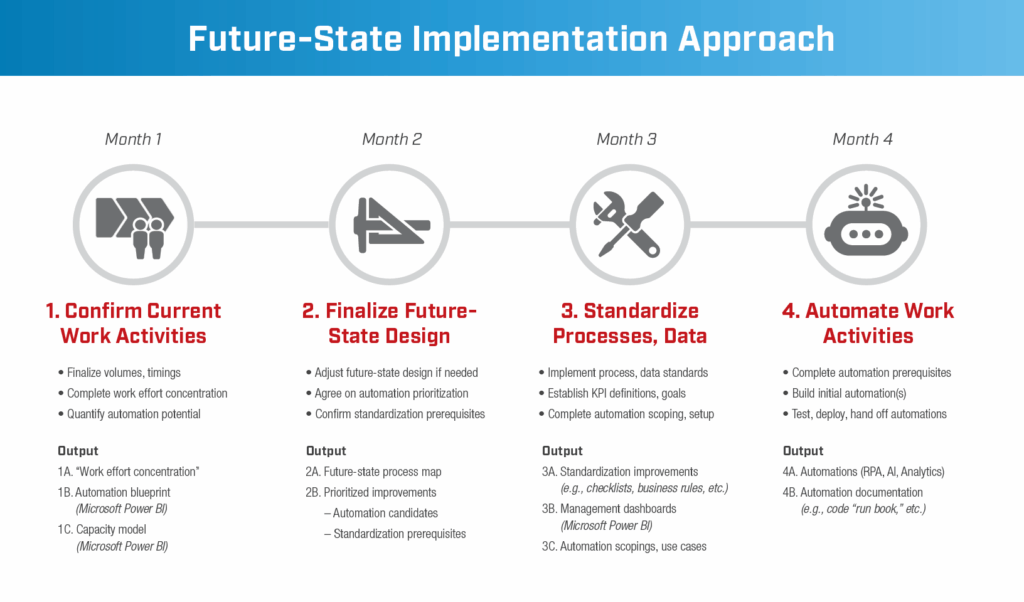

We can break down the answer to this question in four steps:

Step 1: Build a future-state process map

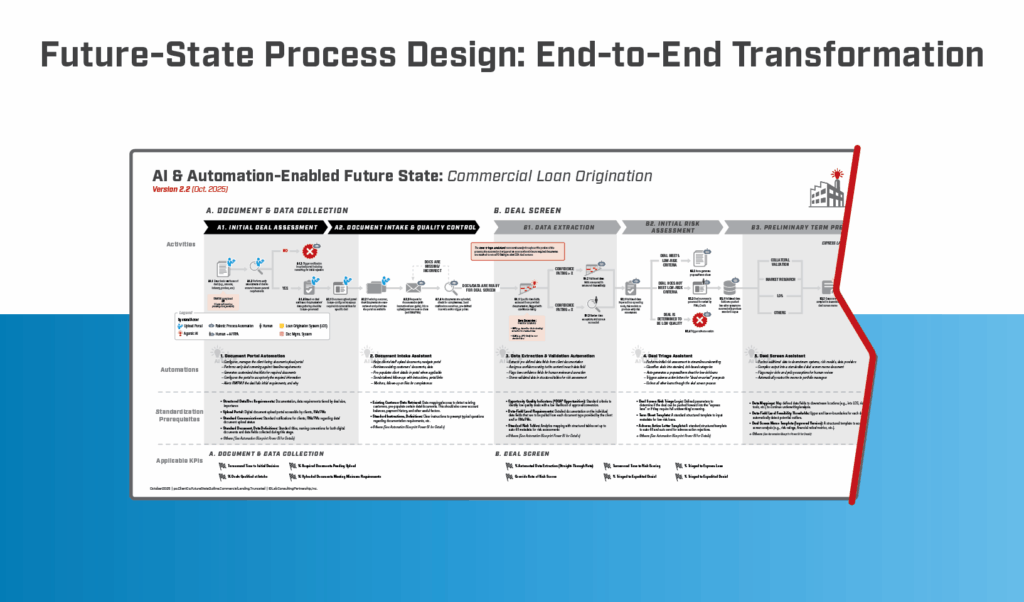

Having a clearly outlined and documented goal of the best-in-class future-state process map is Step 1 for any business and process transformation in banks and credit unions. Design the process with the ideal end-state in mind. Don’t worry about how you’ll do it at this point; just focus on what you want.

Then use the best-practices survey (a key deliverable from current-state process mapping for banks and credit unions performed by The Lab) to identify the gaps to close in achieving the ideal best-practice future state. The result? A clear inventory of improvements to make: Activities to standardize, add (even remove), and automate.

Not sure how to build it? The Lab has best-in-class, time-tested future-state processes pre-built and ready for use in your bank or credit union.

Step 2: Document the gap-closing changes needed

Prerequisites, prerequisites, prerequisites. That’s what this step is all about.

Once you’ve identified your bank or credit union’s future-state goals and inventoried them, the next step is to gap-test them against your current state. Here, you want to identify the prerequisites needed to bridge the gaps:

- Activities performed

- Tools/systems used

- Policies enforced

- Work organization (who does what)

- Required re-engineering to allow for the future-state automation

Specific examples typically include things like:

- Standardized list of documents to collect

- Standard locations, data tables (think: “shelving”) for all the data you’re going to be collecting

- Standardized templates, naming conventions, triaging protocols

Step 3: Organize your information into a standard, automation-ready data model

First, identify the list of Executive KPIs needed to manage performance with this new future state. Next, “walk backward” to identify the data sources, fields, and tags needed to make it automation-ready for data intelligence. Then, using that data (The Lab already has a template to get you started), implement the standard data model.

Want more information about this vital Step 3? The Lab has a complete article about data intelligence, advanced analytics, and Executive KPIs which breaks this crucial Step 3 into a full long-form step-by-step guide.

We also have numerous informative videos (typically about three minutes apiece) about advanced analytics and Executive KPIs in banking and credit unions. Here are a few:

- Retail branch market share analytics video

- Retail branch staffing model analytics video

- Executive KPIs analytics video

- Commercial loan officer productivity analytics video

- Commercial lending sales pipeline analytics video

- Risk and fraud management advanced analytics video

- Collections and charge-offs advanced analytics video

See even more at this full YouTube playlist.

Step 4: Identify the resources and support you’ll need to perform the changes.

As you would in any project-management office, take your goals and requirements list to generate an executable work plan with resources (tools and subject-matter experts or SMEs) to support it for your bank or credit union.

What you’ll need: Champions. You’re going to need SMEs to champion the transformation from each part of the organization. Initially, you’ll want to identify SMEs by line-of-business, and their corresponding teammates in IT. Eventually, the addition of team members from Risk and other departments, jointly reviewing the future state, is key to a successful outcome. But be careful not to over-engineer the process with superfluous layers of approvals and checks. Keep the core team with the business and management. Everyone is important, but their support is for refinements and ways to make things better.

Bonus: What you won’t need. Here’s good news: You won’t need a rip-and-replace of your core, major platforms, systems, loan-origination system (LOSs), and so on. With agentic AI and robotic process automation in banks and credit unions, also known as RPA, automation can be performed on your existing core, systems, and platforms. In other words, AI and RPA are front-end capabilities that work with (and around!) your existing systems to help them do what current platforms can’t do… or can’t do well. This all adds up to great news from a time and budget perspective: No major software or implementation are needed!

3. Are there typical pitfalls and traps that we can avoid as we transform our bank or credit union?

You likely got the hint from Step 4, above: Don’t over-engineer your bank or credit union’s business transformation project, putting technology before process. The pace needs to be pragmatic, agile, and geared toward a lather/rinse/repeat cadence.

Given the importance of a business and process transformation for your bank or credit union, it’s common for over-eager project managers to over-engineer the process, with too many people, too many layers, and too many redundant reviews.

Our advice: Stay away. While it may seem as though all of these are needed to ensure properly implemented improvements, in reality it typically slows everything down, and eventually “clogs the arteries,” blocking the initiative from attaining any goal.

4. How can my bank or credit-union transformation deliver meaningful (and not just theoretical) benefits?

Simply going through the motions of the four steps outlined in Section 2 (“What and where do I need to begin transformation in my credit union or bank?”) won’t automatically drive results. If you want to see the benefits actually realized, you’ll need:

- A complete and detailed budget by target, capability, or deliverable

- Executive sponsorship

- Continuous communication to the organization

These may all strike you as common-sense checklist items, but each one requires conscious, deliberate thought in order to ensure success.

Let’s look at each one in detail.

TOP 5 BENEFITS TO TRANSFORMATION

What are the top 5 benefits of business and process transformation for banks and credit unions?

As we had teased earlier in this article, you should initially focus on three sources of benefits, i.e., where the money in the pocket will come from:

- Waste less/improve productivity.

- Hit more/miss less: Grow deposits and loans.

- Retain more: Preserve your margin.

But there are actually five types of benefits that you’ll enjoy as you and your bank or credit union traverse your business- and process-transformation journey. The following top-five benefits will, together, improve your bottom line while delighting your customers or members:

The Lab Consulting Services

Transformation your bank or credit union today with The Lab

The Lab has helped banks’ and credit unions’ C-suite executives, business and technology leaders, and internal operational-excellence teams to transform their businesses and processes to drive measurable results and deliver successful large-scale transformation initiatives. Our proven comprehensive services and solutions—backed by our industry-leading Knowledge Base of 30-plus years’ worth of templatized, re-deployable client-engagement IP, along with our patented Knowledge Work Standardization® delivery methodology—can transform your financial institution in as little as six to 12 months.

Ready to transform your bank or credit union? To book your 30-minute screen-sharing demo, call (201) 526-1200 or email info@thelabconsulting.com today.