Standardize Your Insurance Business to Increase Performance 24% to 41%

Looking to boost efficiency while implementing agentic AI, RPA, and automated KPI reporting in your carrier, brokerage, MGA, or MGU? Find out how Knowledge Work Standardization® will help you.

As a C-suite executive, technology lead, or part of the internal improvement team at an insurance carrier, brokerage, or agency, your internal transformation strategy depends upon improving operating leverage and scalable capacity.

Fixing the problems requires finding the problems. The Lab has found, during our more than three decades’ worth of client engagements with insurance businesses across North America, that there’s an eye-opening amount of what we call “virtuous waste” taking place in insurance businesses every day. (Our decades’ worth of client-engagement IP has been captured and templatized in our semantic Knowledge Base.)

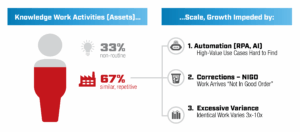

In fact, as you read this, your insurance white-collar workforce, a.k.a. its “knowledge workers” will spend (“squander”?) a full 35 percent of their day, today, on wholly nonproductive activities such as duplicative effort, fixing errors, and over-serving policyholders.

Why is this effort called “virtuous” waste? It’s because the people who are doing it, think it’s helping, not hurting, the organization. They regard it as totally unavoidable in insurance; in fact, they think it would be wrong not to do it, believing it’s essential for providing proper policyholder service. As an insurance executive, you see this as a cost. They don’t. Nor do their managers.

Clearly, this “assumed truth” is detrimental to achieving increased operational efficiency in insurance. So don’t assume that these “truths” are true. Challenge them. In so doing, you can re-capture earnings of 20% or more.

What, then, are these “assumed truths” in insurance operations that you should confront and dismantle? They are:

- Assumed Truth in Insurance Number 1: “The knowledge work in our brokerage, carrier, or agency operations cannot be standardized.” They think it can’t be standardized, but we know—as you will, by the time you finish reading this article—that nothing could be further from the truth. In fact, some 67 percent of today’s knowledge-work activities in insurance can—and should—be standardized. You read right: Two-thirds. It’s a substantial opportunity.

- Assumed Truth in Insurance Number 2: “Our insurance business and its processes are unique, so they can’t be standardized.” Of course your insurance business isn’t identical to your peers’ businesses… but tons of its components virtually are. We’re talking about org structure, big processes like quote-to-bind and claims processing, along with all of their constituent work activities and tasks. They’re not unique.

- Assumed Truth in Insurance Number 3: “We can simply entrust new core technology to automate our insurance operation.” Not so fast. Until you’ve eliminated all of the “virtuous waste,” you’re at risk of just moving bad work from one core system (such as your agency management system or AMS) to another. Good news: Three-quarters of knowledge-work improvements can be achieved with existing core technology.

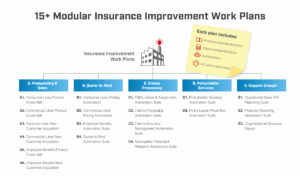

In this article about standardization in insurance for carriers, brokerages, MGAs, and MGUs, we’ll review The Lab’s patented Knowledge Work Standardization methodology, and how it:

- Spotlights and decreases virtuous waste

- Increases productivity

- Paves the way for technologies such as agentic AI, robotic process automation (RPA), and Executive KPI data analytics with automated reporting and custom-generated “to-do lists” of corrective actions

How do you define “standardization” of knowledge work in insurance?

How to put process before technology when standardizing insurance operations

Here is a good working definition of Knowledge Work Standardization in insurance:

“Knowledge Work Standardization in insurance is a process-before-technology methodology which employs a standards-focused approach to organizational strategic transformation and improvement in carrier operations, brokerages, and agencies such as MGAs and MGUs.”

If, as an insurance executive, you’re looking to introduce technologies such as data intelligence, AI, predictive analytics, and the onboarding of a digital workforce/automation, know that standardization must precede all of those introductions. It’s the only way to ensure enterprise-wide benefits from those technologies.

Why standardize? Here’s the business case for your insurance operation

What are the 3 top benefits of standardization in insurance?

Glad you asked. When you standardize your insurance operations, you can:

- Win more, and more profitable, policyholders. When you’ve standardized your insurance operation, you’ll have newfound market insights, which translate to improved market/customer segmentation, improving cross-sell and upsell to existing policyholders, while informing more productive prospecting.

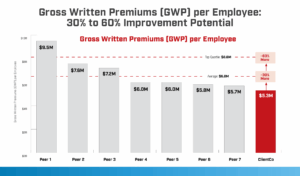

- Increase productivity: Waste less, with productivity gains of 24% to 41%.

- Retain more margin—up to 2.5 points.

Check out The Lab’s classic Knowledge Work Standardization overview video. It’s entertaining and informative.

Do you know the five “W’s” of operational standardization?

Defining the “who, what, and why” of insurance standardization

Be sure to check out The Lab’s informative long-form article about transforming your insurance carrier, brokerage, MGA, or MGU. It lists numerous benefits of transformation; think of “standardization” as the prerequisite for all of them.

There are basically five “W-based” questions which your insurance standardization initiative should ask and answer, namely:

- Who is being standardized? Answer: Every single insurance function (and person within it) which the end-to-end process (and data) goes through.

- What is being standardized? Answer: All of your E2E or end-to-end processes and data.

- Why is it being standardized? Answer: As noted above, it’s the best-practice essential for delivering the most benefits from insurance transformation.

- Where is it being standardized? Answer: Everywhere. You need to include each system in every end-to-end process, as well as the data it uses.

- When is it being standardized? Answer: Preferably ASAP. Fortunately, The Lab’s patented Knowledge Work Standardization methodology can deliver standardization for your insurance operation in as little as six to 12 months.

How to avoid pitfalls when standardizing insurance operations

What is the biggest obstacle to insurance standardization?

When people demand, without factual basis, more information than is required, that’s known as the false precision trap. In short: False precision is a pitfall to avoid when standardizing your insurance business.

As noted in The Lab’s long-form explainer article about process and customer journey mapping in insurance, you need the right amount of precision. Just as you’ll want to map your current-state, you needn’t map 100% of it, any more than you should quantify every single improvement opportunity. That’s too much; it’s false precision.

What, then, is the cut-off? You want to look upstream in the process. See what needs to be standardized. Don’t worry about measuring how long each process lasts or other similar false-precision “requirements.”

How should you define standardization in insurance scope and goals?

What should I standardize in my insurance carrier, brokerage, or agency?

To achieve E22 (a.k.a. end-to-end) standardization in insurance, you should standardize not just the activities and workflow but also the data. You’ll want to “dig down to bedrock,” and identify activities at the 3- to 5-minute detail level.

You’ll need to standardize all of the data, and how it’s used, in each activity. These are typically referred to as “Level 4” work activities and data.

For each activity, be sure to:

- Map each constituent task to grasp its detail.

- Inventory the work-effort concentration (WEC).

- Map each future state.

For the data used in each activity, be sure to:

- Source it.

- Define it.

- Data-model it.

In so doing, you’ll render it automation-friendly, as well as future-state optimized.

What are the most valuable benefits of standardization for P&C insurance?

List of the 5 biggest benefits from standardizing insurance operations and data

There is no shortage of value drivers when it comes to bringing standardization best practice to your insurance carrier, brokerage, or agency. Here are the top five:

Benefit 1 from Standardizing Insurance: Data “conversations.”

It sounds like science fiction, but with standardization in insurance, it actually becomes quite easy to chat it up with your data. You can ask questions whenever you want—in English—and get actionable replies, also in English. You can also have data pushed out to you automatically, at intervals or thresholds of your choosing.

Benefit 2 from Standardizing Insurance: Improved compliance and risk management.

When you eliminate variance among your insurance processes and data, you’ll fortify your audit trail while reducing risky errors. Processes can become RPA automated, repeatable, predictable, and transparent.

Benefit 3 from Standardizing Insurance: Automate more than you can imagine.

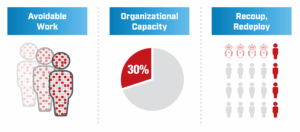

Once you standardize your insurance operations and data, you’ll be able to automate some 30 – 50% of activities, with people and bots working together. And the more you automate, the more benefits there are.

Benefit 4 from Standardizing Insurance: Elevate the policyholder experience.

Get ready to surprise and delight your customers. With insurance automation, you can provide smooth, seamless policyholder interactions at every single touch-point. And by reducing friction (think hold times or redundant forms), you’ll improve your relationships with policyholders, too.

Benefit 5 from Standardizing Insurance: Increase scalable capacity.

Standardizing is the key to the full potential of your workers. They’ll have better, more satisfying work to perform, leading to higher retention. With standardization in insurance, your carrier, brokerage, or agency will become a coveted place to work, attracting the top candidates for you to choose from.

What are the steps for standardizing insurance operations?

How do I standardize my insurance business?

We can break down the process of standardizing your insurance business into six discrete steps:

Standardizing Step 1 in Insurance: Create current-state process maps. You’ll need to first map out all of your as-is, end-to-end knowledge work activities and customer/policyholder journeys. The Lab specializes in process mapping for insurance businesses; we can map your operation in just six to eight weeks. Be sure to read our great article about process mapping for insurance.

Standardizing Step 2 in Insurance: Classify insurance work activities. While you’re working on your process map, you’ll need to categorize your insurance knowledge-work activities into an enterprise-wide system of classification, also known as a taxonomy. Add tags to the different activities, indicating:

- Work volumes

- People/roles who perform the work

- Time required for different activities

The Lab has pre-built templates to facilitate this step.

Standardizing Step 3 in Insurance: Draft the to-be process map. Counterintuitively, you’ll need to set your as-is process map aside for the time being. Instead, create an optimum to-be wish-list of what you seek to accomplish in your insurance business in the future. At that point, you can compare and contrast it to the as-is map and taxonomy you’d already created.

![]()

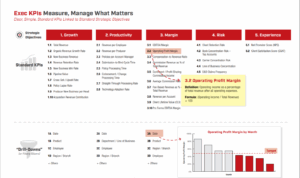

Standardizing Step 4 in Insurance: Create Executive KPI definitions. To measure and monitor future-state performance in insurance, you’ll require executive-level KPIs or Key Performance Indicators.

The Lab’s popular KPI Handbook For Insurance contains more than 300 industry KPI definitions. These span prospect-to-quote, quote-to-bind, claims from FNOL through recovery, and many more. In fact, they’re grouped by their impact on productivity, cost, revenue, service, volume, and other factors.

At this point, however, you’ll want to start with the essential few Executive KPIs, sometimes known as Super KPIs in Insurance. Find those from The Lab right here, as well. These are all about growing premiums, preserving margin, and increasing productivity and efficiency.

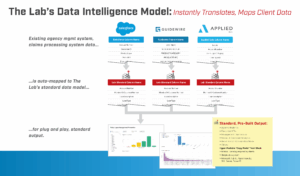

Standardizing Step 5 in Insurance: Locate the sources of all data. Each insurance data element is fed from multiple different sources. Determine the “feeder” parts of each, identifying its source, from every system, platform, and repository in your insurance operation.

Standardizing Step 6 in Insurance: Data standardization. After you’ve ID’ed the data sources, you’ll need to ETL, or extract/transform/load it into The Lab’s Standard Data Model. Fortunately, The Lab’s templates make this step surprisingly easy to perform.

What are the top requirements for standardization in insurance?

Three essential needs for getting the most value from insurance standardization

Here are the three things which C-suite executives must ensure, in order to derive the maximum value from their insurance-standardization initiatives:

- Don’t standardize “by business.” Standardize “by process.” That’s a big difference. It lets you “follow the process,” while clearing any artificial hurdles imposed by turf wars, inter-departmental politics, and other rice bowls.

- Name your “champions of process.” Designate well-regarded peers to make sure your insurance standardization initiative meets success vs. pushback.

- Shout it from the rooftops. Make your insurance standardization effort a top-three enterprise priority. Make that known, enterprise-wide. Share wins. Push out videos. Promote standardization in your intranet, your newsletters, your town halls, and emails directly from the CEO.

Understanding The Lab’s insurance standardization services

How can you standardize insurance operations with The Lab?

The Lab’s diverse services reflect our wide-ranging capabilities for insurance leaders. These include data standardization, process mapping, and templatized solutions for automation and AI, process improvement, and analytics. Regardless of where your carrier, brokerage, or MGA/MGU resides on its standardization-in-insurance journey, The Lab can help, with best-practice implementation, rapid rollout, and maximum ROI.

If you’re ready to standardize your insurance business, schedule your demo with The Lab. Simply call (201) 526-1200 or email info@thelabconsulting.com today.