Finally—a way to liberate your bank from “core” competitive restraints with digital transformation bots

A recent survey of community-bank CEOs asked them to choose the biggest threat to their growth prospects. Can you guess what it was?

- Think it was competition from other banks? Nope.

- Think it was competition from non-bank companies? Nope.

- Think it was the challenge of recruiting and retaining talent? Nope.

- Think it was regulatory mandates? Nope. Not even close.

The one thing that all of these bank CEOs agreed on—what they clearly perceived as the biggest threat to their growth prospects—was the inability for them to innovate, due to constraints from their core platform and its provider.

That bears repeating. Bank CEOs agree that their own core-system providers pose the biggest hurdle to their growth, efficiency, and operating leverage.

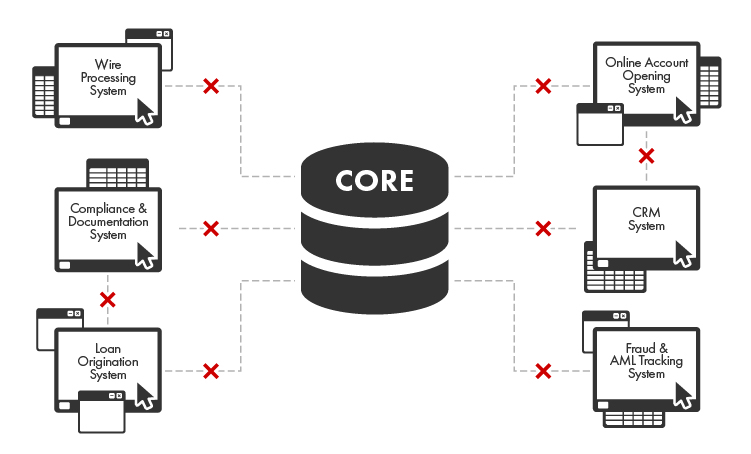

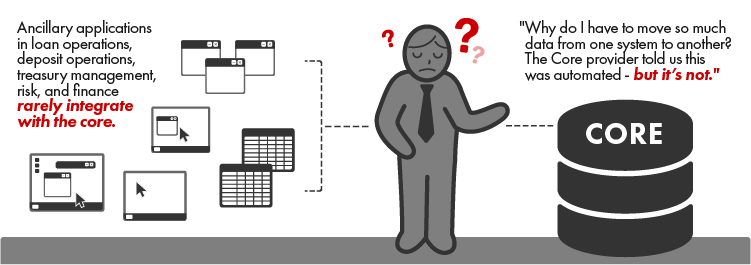

It’s a sad fact, but it’s hardly shocking. The few core-system providers—and you know who they are—operate more like private-equity firms than tech companies. They’ll buy up the latest company du jour and stamp their logo onto its offerings. But they certainly won’t integrate it. They don’t update it. As you well know, they’ll have lots of different core systems, but none of them talk to each other, forcing you to park a highly-paid human between them as the “glue” that holds the whole thing together.

To their credit, these core-system providers are good at one thing: Raising prices.

Little wonder all of the country’s bank CEOs are so frustrated.

The more things change…

At The Lab, we see—and help banks to confront—this challenge all the time. Interestingly, it’s a mix of old (as in “never-changing”) and new. On the “old/never-changing” side, it’s activities that banks perform, by the thousands, daily: Things like processing ACH stop payments or outbound wires. On the “new” side, it’s issues like PPP loan processing—and then the subsequent forgiveness processing, with the SBA changing (sorry, “updating”) their requirements virtually week-to-week.

Running your bank is hard enough. It’s doubly frustrating when the very tools you rely on to run your business actually hobble its ability to operate, let alone grow.

And the problem isn’t going away. To the contrary, it’s only getting bigger. The core-system providers have no incentive to change their business models; they’re an effective oligopoly. And there will always be new legislation and new regulations that force you to keep current: Let’s say there’s new anti-money-laundering (AML) requirements on the horizon. There may be a little company that pops up with a “solution” for it. But how do you integrate that? The core providers may actually buy that company—but they won’t integrate it, either.

Not only do your headaches (and liability exposure) increase, but you’re also forced to staff up, just to keep up. It’s a dismal prospect.

Free your workers from the nightmare

For every cluster of open-this-system/compare-this-to-that activities (commonly known as “reconciliations”) that your bank’s knowledge workers are struggling with, you’re paying the price in terms of lost productivity and morale.

But there is a way out of this trap. The Lab helps banks with this all the time.

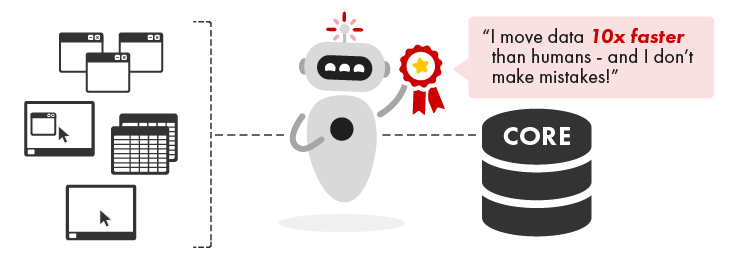

The answer: Robots.

Robotic process automation, or RPA, allows you to “park a bot” on top of a human “sit-at-the-computer” activity and automate it. It’s not a core system. In fact, there’s no IT intervention. Think of the bot as just another worker: one with their own log-ins and passwords, able to “sit at a computer” all day and type, click, compare, copy, and paste. Except they work at blazing speed. They never get tired. They never make mistakes. And they can be updated just as quickly as regulations change.

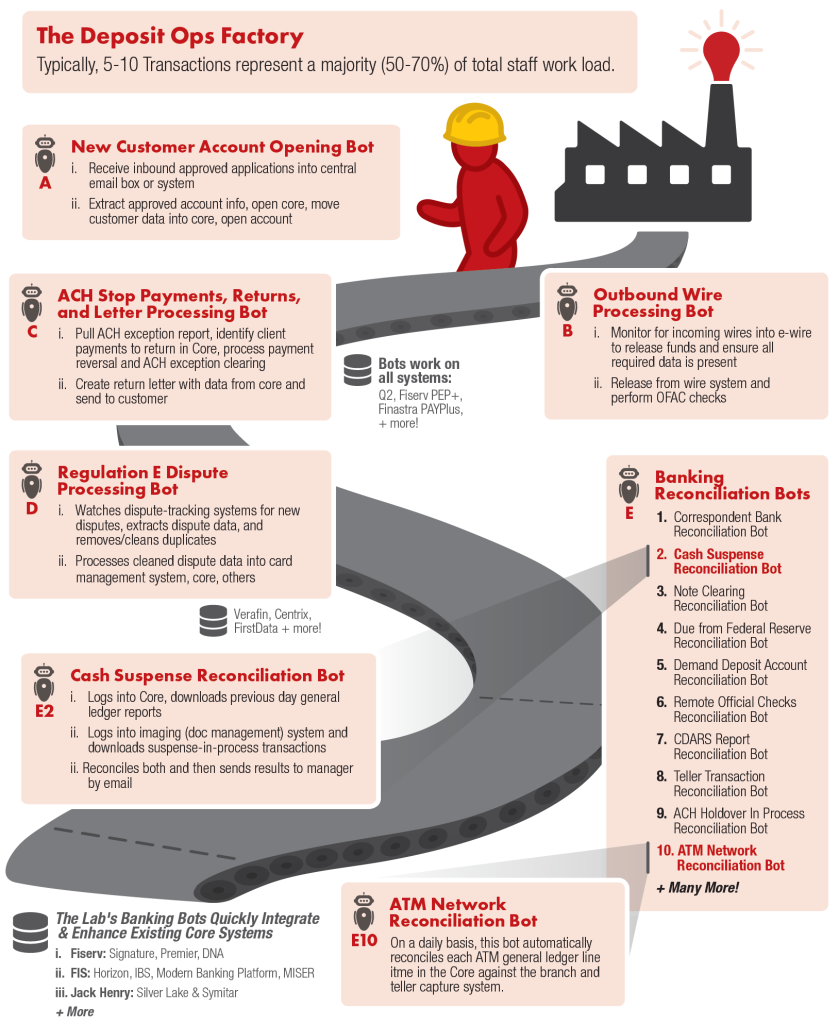

If you’re new to RPA, you’ll need about a half dozen bots in order to get started. The back office is a great place to get started. Here are some examples of banking-bot clusters which The Lab routinely installs; note that these would be customized for the exact way you get things done—and for the multiple core systems (and other ancillary systems) you use to complete them:

- The Reg E Debit Card Fraud Processing Bot Suite. The name says it all, doesn’t it? Today, you have a human worker—no, make that “lots of human workers”—assigned to this chore. You need to identify disputes in the processing queue from the dispute management system. Then you must find the corresponding transactions in the core system. Then you need to confirm the completion of the dispute forms, then adjust them in the core and a document management system, and attach notes. Then there’s the pulling of the daily transaction report, updating a balance reconciliation spreadsheet, verifying the transactions in two different core systems…. Are your eyes glazing over yet? We haven’t even finished. We’ll skip the rest of the grueling details, but suffice to say, this little “bot suite” will save a mid-sized bank about 3,000-6,000 hours per year of expensive, mindless, error-prone human activity.

- The Outbound Wire Processing Bot Suite. Three core provider systems which don’t talk to each other. A shared repository which resides outside the cores. A common process that consumes about 4,000-20,000 error-prone hours per year, depending on the size of the bank. All of the in-the-weeds details of verifying transactions via email, properly completing required form-fields, populating templates, awaiting dual-control releases…. It’s a scenario that’s built for bots.

- ACH Stop Payments Bots. The interesting thing about this all-too-common chore is how many different ways it can be done by different banks. At The Lab, we’ve seen them all. Some use just a few core systems; others use lots. There are different ways of papering the audit trail; need a screen-shot of a transaction? Let a bot do it. In fact, let a bot do all of it. A suite of “Stop Payment Bots” will pay for itself in short order—and free your knowledge workers for higher-value activities.

Bank 1 – ACH Stop Payment Bot

https://www.youtube.com/watch?v=KrrLrxzPnEM&t=95s

Bank 2 – ACH Stop Payment Bot

- PPP Bots—processing, forgiveness, and beyond. Back when banks were overwhelmed by PPP loan applications, The Lab stepped in to help them with the application intake, eligibility scoring, uploading to the SBA portal (even when it timed out a ton), and more. We automated 100,000+ loans with bots. Now, “forgiveness” requires the same process all over again. It’s simply wasteful to do this without bots. But here’s the bigger story: Every bot application from the PPP program applies to all of your bank’s lending activity. This story is far bigger than the PPP program. It’s a game-changer.

Install a bot “factory” in your bank

Every cluster of back-office operations at your bank is simply begging for a suite of bots to “factory-ize” it. Take a look:

Want to beat the core-system-provider blues? Contact The Lab today. We’ll show you how we can install bots, start to finish, in just weeks… and how we’re able to do it all remotely from our offices in Houston. Simply call (201) 526-1200 or email info@thelabconsulting.com to book your no-obligation 30-minute screen-sharing demo today!